CustomsGenius

CustomsGeniusIEEPA Tariff Refund Eligibility Explained

If you buy imported goods through a third-party importer, wholesaler, or manufacturer, here’s a question that deserves immediate attention: once the importer of record collects a refund of IEEPA tariffs from the government, does your company have a right to part of that money?

This alert speaks directly to retailers, distributors, and other purchasers who are not the importer of record but who absorbed IEEPA tariff costs through higher prices. We walk through the current state of the IEEPA refund process, explain why it has financial consequences for companies that never interacted with Customs, and outline the contractual and legal strategies available to recover the portion of those refunds that corresponds to tariff costs you already paid.

A Key Caveat: How the government will distribute IEEPA tariff refunds remains an open question. Any downstream claim depends on the importer first collecting its money from the government. That process is underway - and buyers should be watching it closely.

The Pass-Through Problem

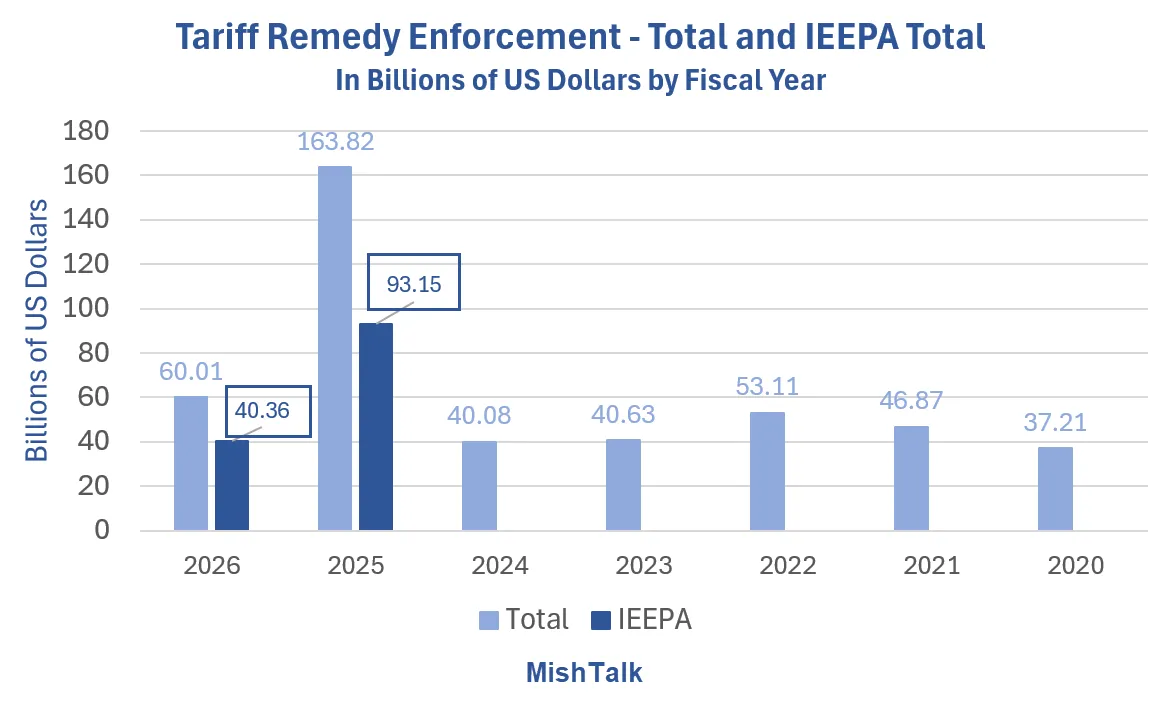

When IEEPA tariffs were in effect, importers of record paid significant duties to the government. Most did not eat those costs. Instead, the tariff burden flowed downstream in the form of higher prices - sometimes broken out as a tariff surcharge, sometimes folded into a general price hike. The result was the same: downstream buyers bore the economic weight of the tariff.

The Supreme Court’s ruling in Learning Resources, Inc. v. Trump now opens the door to refunds for those tariffs. But here’s the catch: the refund goes to the importer of record - the party that paid Customs. If the importer already passed those costs along to you, the refund represents money recouped twice: once from you, and once from the government. Unless downstream buyers speak up, that double recovery stays with the importer.

The Channels Importers Are Using

Importers have multiple routes to recover IEEPA tariffs, depending on where their entries stand in the Customs pipeline. Entries that have already been liquidated can be challenged through a formal protest under 19 U.S.C. § 1514, with a 180-day filing window from the date of liquidation. Entries still awaiting liquidation can be corrected through a Post-Summary Correction (PSC) submitted via the Automated Broker Interface. When administrative options are unavailable or exhausted, importers can bring suit at CIT, the court with exclusive authority over federal import disputes.

Many importers with substantial exposure are already moving through these channels. For downstream buyers, the moment the importer collects a refund is the moment your recovery clock begins.

Evaluating Whether You Have a Claim

Recovery isn’t automatic. The strength of a downstream buyer’s position depends on several evidentiary factors.

The clearest scenario is one where your supplier explicitly told you prices were going up because of IEEPA tariffs. Written communications - emails, formal notices, revised price sheets - that tie price increases directly to the tariff create a documented chain linking the government duty to the cost you paid. This kind of evidence is the most compelling.

Contracts built on cost-plus or open-book models also create a strong basis for recovery. When an importer’s actual costs, including duties, feed directly into invoice pricing, a tariff refund retroactively lowers the cost base. The pricing mechanism itself may require an adjustment.

Even without direct documentation, a pattern of prices rising in tandem with tariff imposition - and falling when tariffs were removed - supports a reasonable inference that pass-through occurred. This kind of circumstantial evidence gains strength when paired with other indicators.

Separate tariff line items on invoices or purchase confirmations are especially useful. They create a clear paper trail showing that duty costs were itemized and charged to the buyer.

Finally, in industries where pass-through was pervasive, broader market evidence - trade group reports, press coverage, government studies - can fill gaps even where a particular supplier didn’t provide explicit documentation.

What Your Contracts May Already Provide

Existing agreements may contain provisions that support a recovery claim. Duty drawback sharing clauses are the most direct: they obligate the importer to share refunds with the buyer proportionally. Price adjustment or true-up mechanisms that trigger when underlying costs change could also apply here - a tariff refund arguably changes the cost basis. Definitions of “cost” in cost-plus arrangements that include duties mean a refund should automatically lower the price. Most Favored Pricing provisions that guarantee the buyer access to the supplier’s best terms may be activated when the supplier’s effective cost drops. And renegotiation clauses triggered by material changes in cost structure could give buyers leverage to demand a credit.

What Future Agreements Should Include

Any new supply contract for imported goods should address tariff refund sharing head-on. Buyers should push for:

- A requirement that the supplier disclose any tariff refund, drawback, or remission within a set timeframe (such as 30 days).

- A clear formula tying the buyer’s share to the documented tariff component in purchase prices.

- A defined payment or credit schedule, with interest for late remittance.

- Audit rights covering the importer’s Customs filings, liquidation records, and refund documentation.

Legal Theories When the Contract Is Silent

Contracts don’t always address this scenario - but that doesn’t leave buyers without recourse. If the agreement contains relevant provisions like drawback clauses, price adjustments, or good-faith obligations, a straightforward breach of contract claim is likely the strongest path. Damages are relatively easy to calculate, and the evidentiary standard tends to be favorable.

Where the contract doesn’t cover tariff refunds, unjust enrichment offers an alternative. The argument is simple: the importer received a benefit - the refund - that corresponds to a cost the buyer already paid. Letting the importer retain the entire amount without sharing it would be inequitable. Most U.S. jurisdictions recognize this claim, though some limit it to situations where the contract is silent or ambiguous on the relevant issue.

There is also an argument under the implied covenant of good faith and fair dealing, which UCC Article 2 attaches to every sale-of-goods contract. If the business relationship involved transparent tariff pass-through and the importer quietly pockets a refund of those same costs, a court may find that conduct violates the implied duty of fair dealing.

Steps to Take Now

Downstream buyers shouldn’t wait. Go through your supply agreements and flag any provisions related to tariff pricing, drawback sharing, cost adjustments, or good-faith obligations. Pull together all documentation: price increase notices from suppliers, invoices that reference tariffs, purchase order records, and any communications linking price changes to IEEPA duties. Keep tabs on what your importers are doing in the IEEPA refund process - if they’re filing protests, submitting corrections, or litigating at CIT, refunds may be on the horizon. Put your key suppliers on notice now with a written letter asserting your right to share in any IEEPA tariff refund tied to goods you purchased. And bring in legal counsel who understands both customs law and commercial disputes - tracing the economic flow of tariff costs across a supply chain involves real evidentiary complexity.

Keep in mind: your claim depends on the importer actually receiving its refund first. The IEEPA refund process at the government level is still taking shape, and the rules continue to evolve. But the companies that prepare now will be in the strongest position when refunds start flowing.

Conclusion

The fall of IEEPA tariffs has opened a meaningful recovery window for downstream buyers. Importers that charged their customers for tariff costs - and that are now in line to get those costs refunded by the government - stand to collect twice unless their customers take action.

Our team is helping clients navigate the IEEPA refund process and develop recovery strategies tailored to their supply chains. Reach out if you’d like to discuss your position.

Tracking your IEEPA tariff exposure? Get started with CustomsGenius to centralize your entry data and monitor refund deadlines.

For a complete overview of the refund process, read our guide: IEEPA Tariff Refund: What Importers and Brokers Need to Know in 2026.